Paper checks are supposed to be a relic. And yet, across payroll, vendor payments, rent, and contractor invoices, they remain one of the most trusted payment methods in North American business. The problem was never that businesses wanted to keep writing checks — it's that the tools available to do it were stuck decades in the past: desktop software, single-user, disconnected from banking, disconnected from accounting, and completely unaware of anything happening outside its own little window.

Teams were left stitching together spreadsheets, physical checkbooks, and separate mailing trips just to pay a vendor. There was no shared visibility across a team, no audit trail when something needed to be traced back, and absolutely no connection between the check someone wrote on Tuesday and the accounting software that needed to know about it by Friday. The goal of this project was to take that entire, fragmented workflow and rebuild it as a single, modern, cloud-based product — one that could handle real money, real compliance requirements, and real teams, without ever feeling like "accounting software."

Trust, Built Into the Login

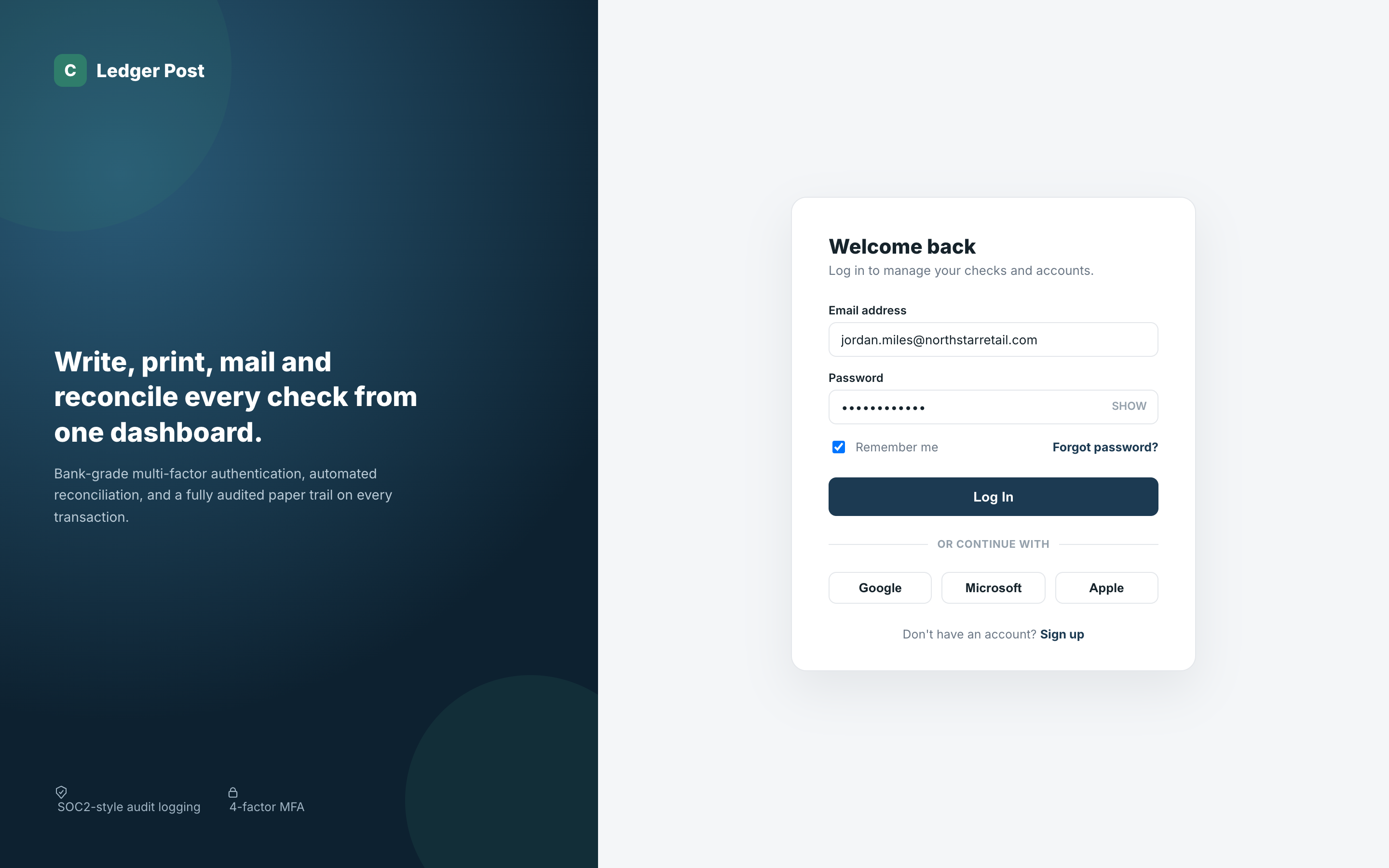

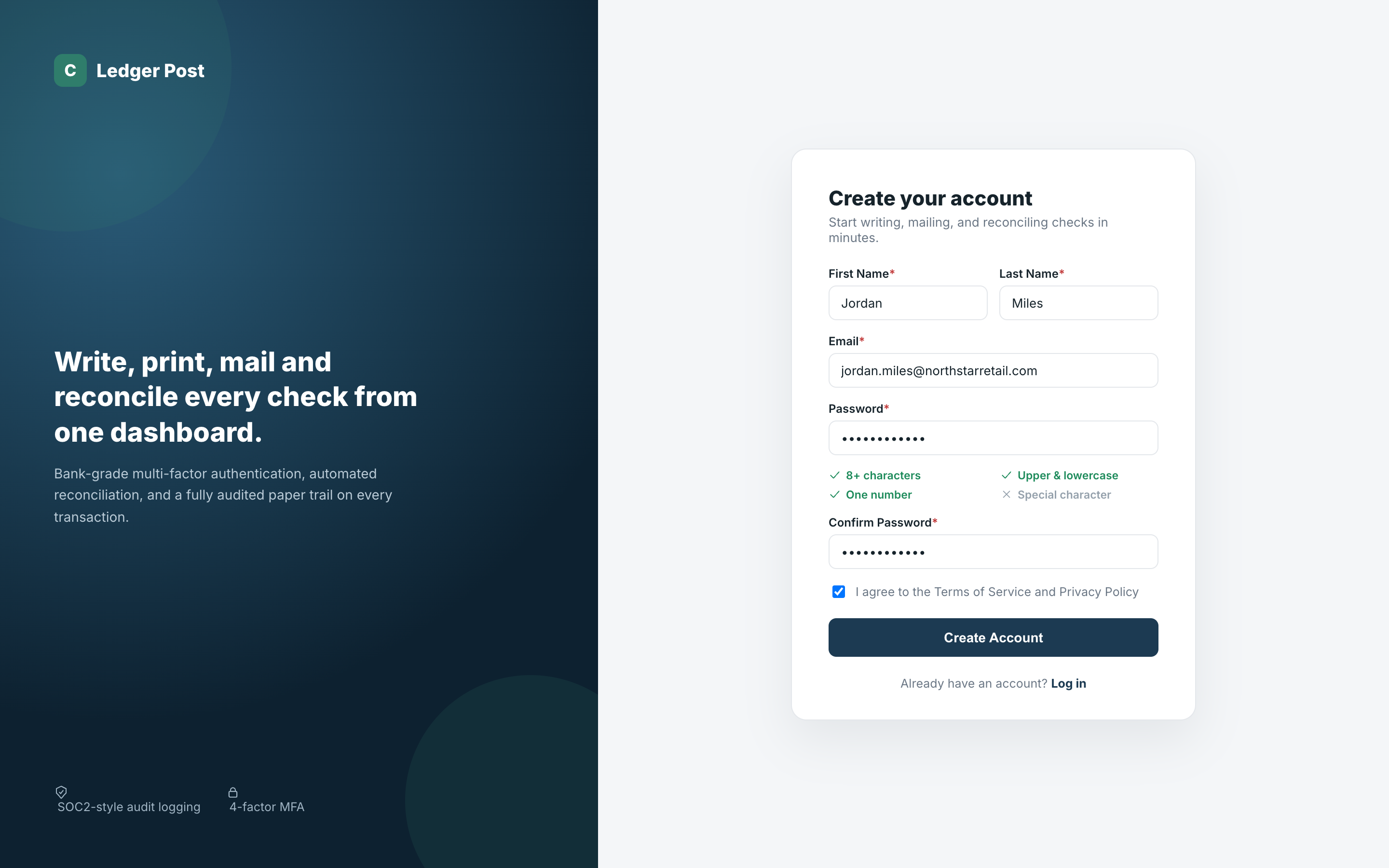

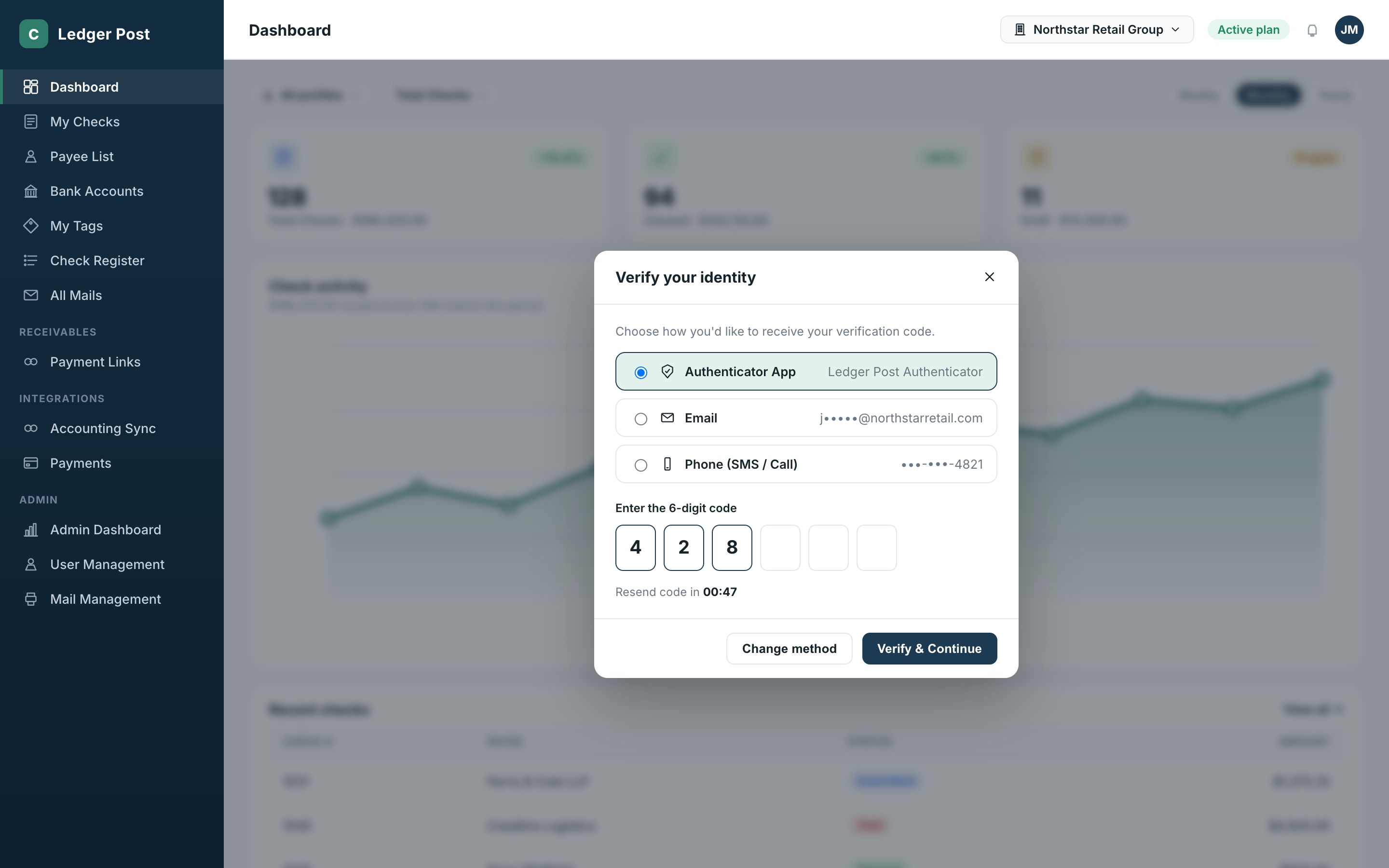

The first design decision was about trust. This is a product that touches real bank accounts and real money, so the interface needed to feel secure without feeling hostile. Login and signup are clean, minimal, and built around clear password guidance rather than cryptic error messages — and every account is protected by mandatory multi-factor authentication, with a choice of an authenticator app, email code, or even a spoken code delivered over a phone call, so no one gets locked out because their preferred channel isn't available in the moment.

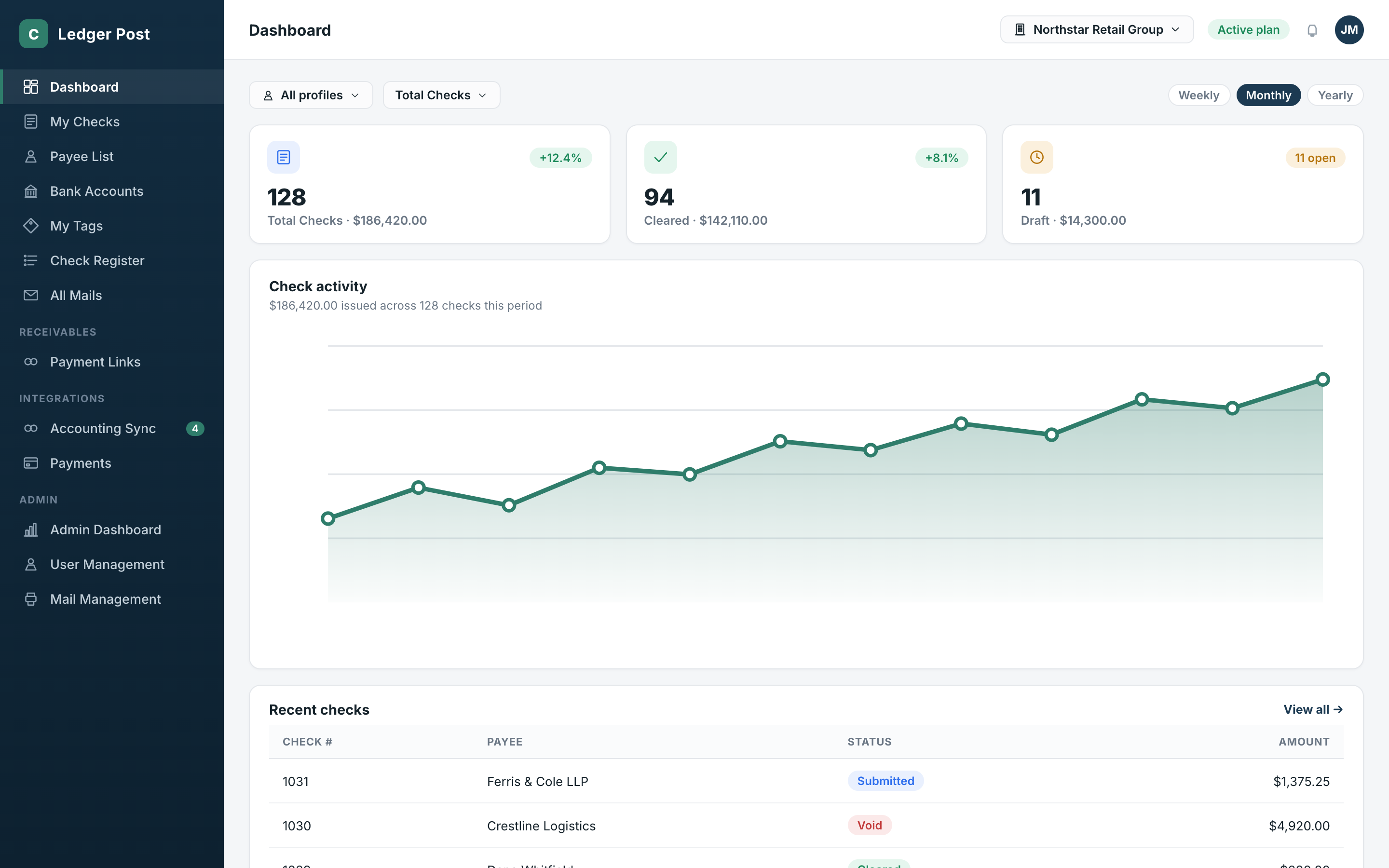

Once inside, the dashboard is designed to answer one question immediately: where does my money stand right now? A running total of checks issued, what's cleared, what's still in draft, and a simple chart of activity over time — all before the user has to click into anything else.

Reconciliation Made Automatic

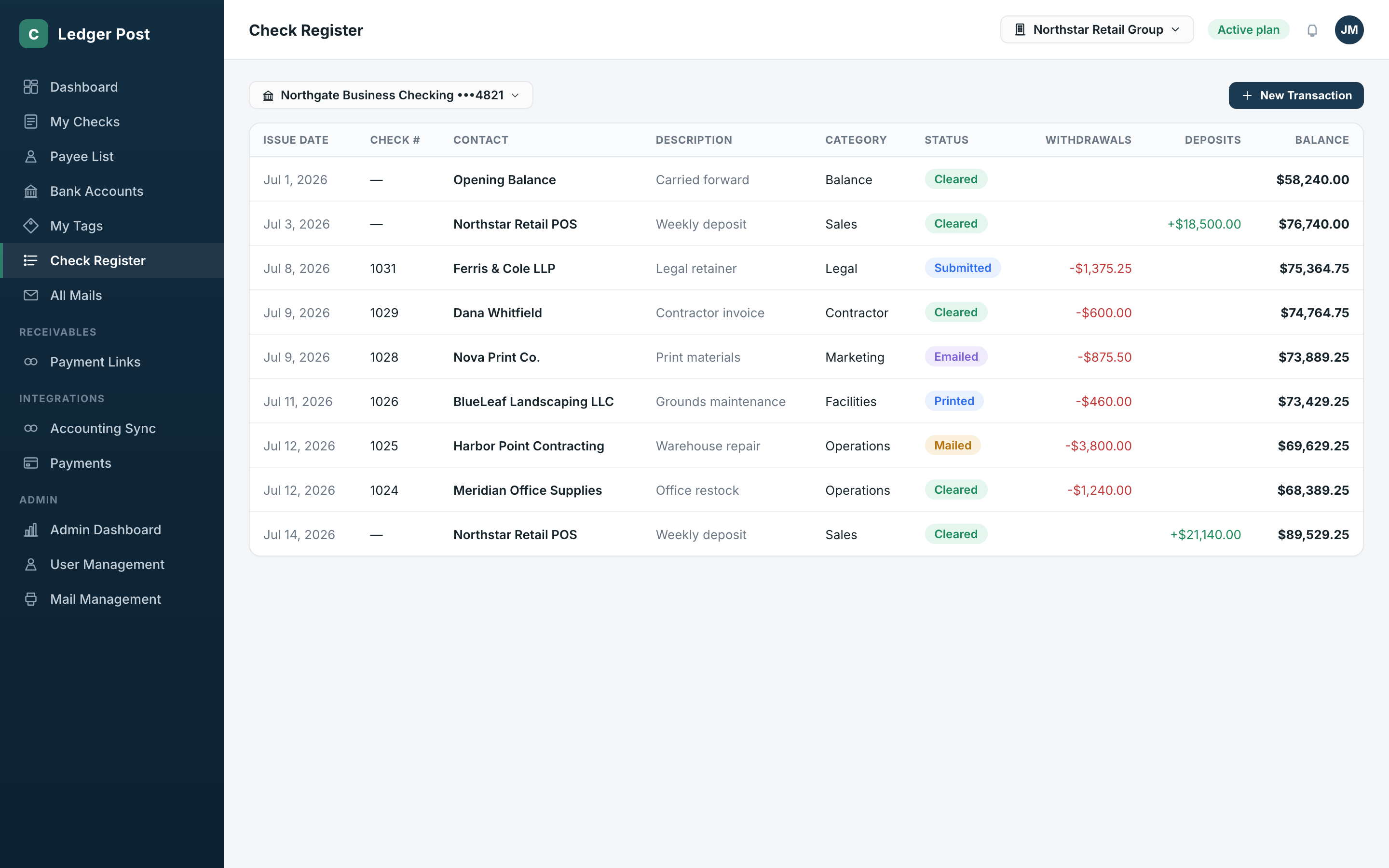

The part of the old workflow that businesses hated most was reconciliation — manually checking off which checks had cleared and recalculating a running balance by hand. This platform treats that as something the system should simply never let get out of sync.

The moment a check is created, edited, or voided, the check register updates itself, showing every deposit and withdrawal against a running balance, the same mental model as a paper checkbook, minus the arithmetic.

The Core Workflow: Writing, Printing, and Mailing Checks

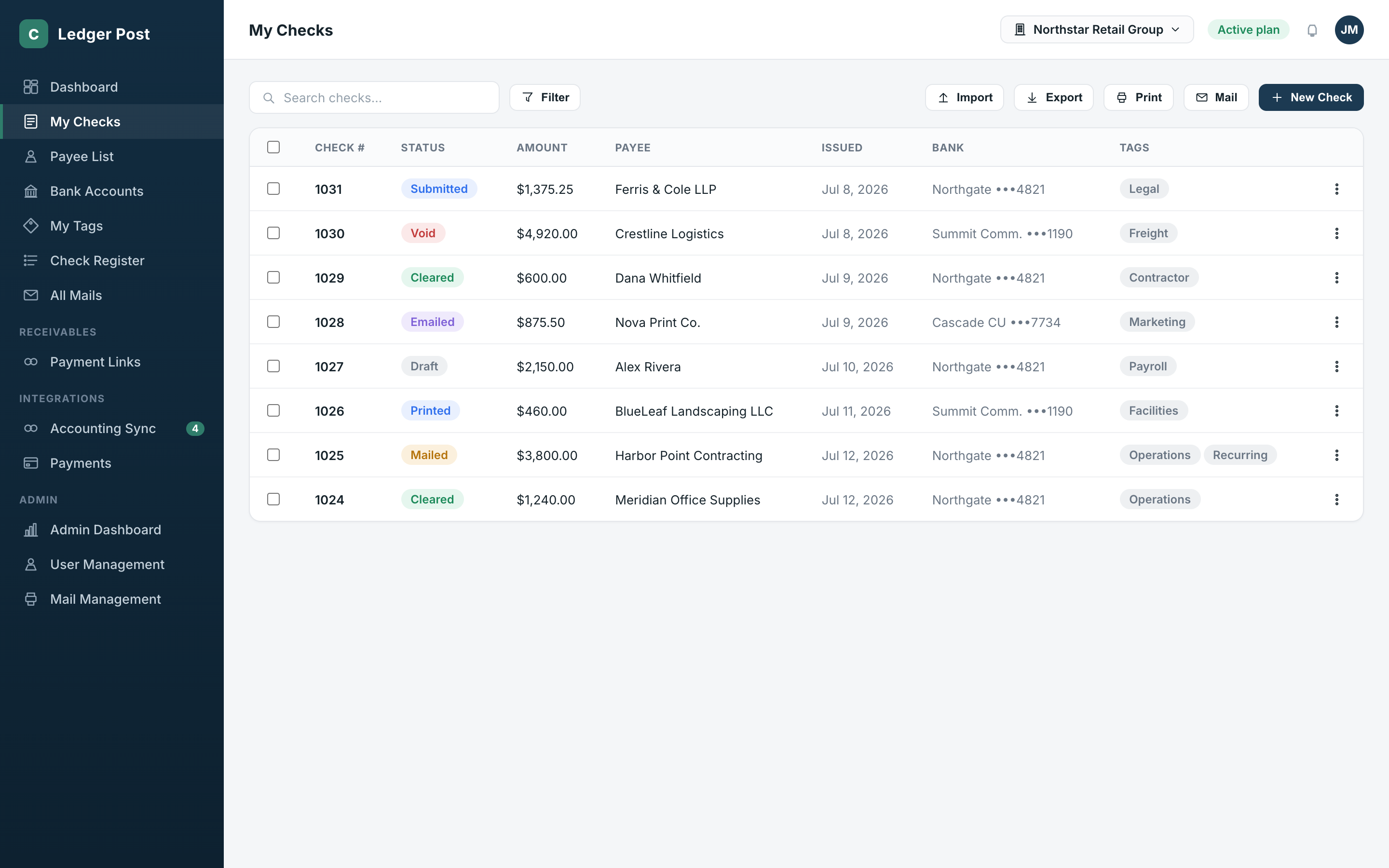

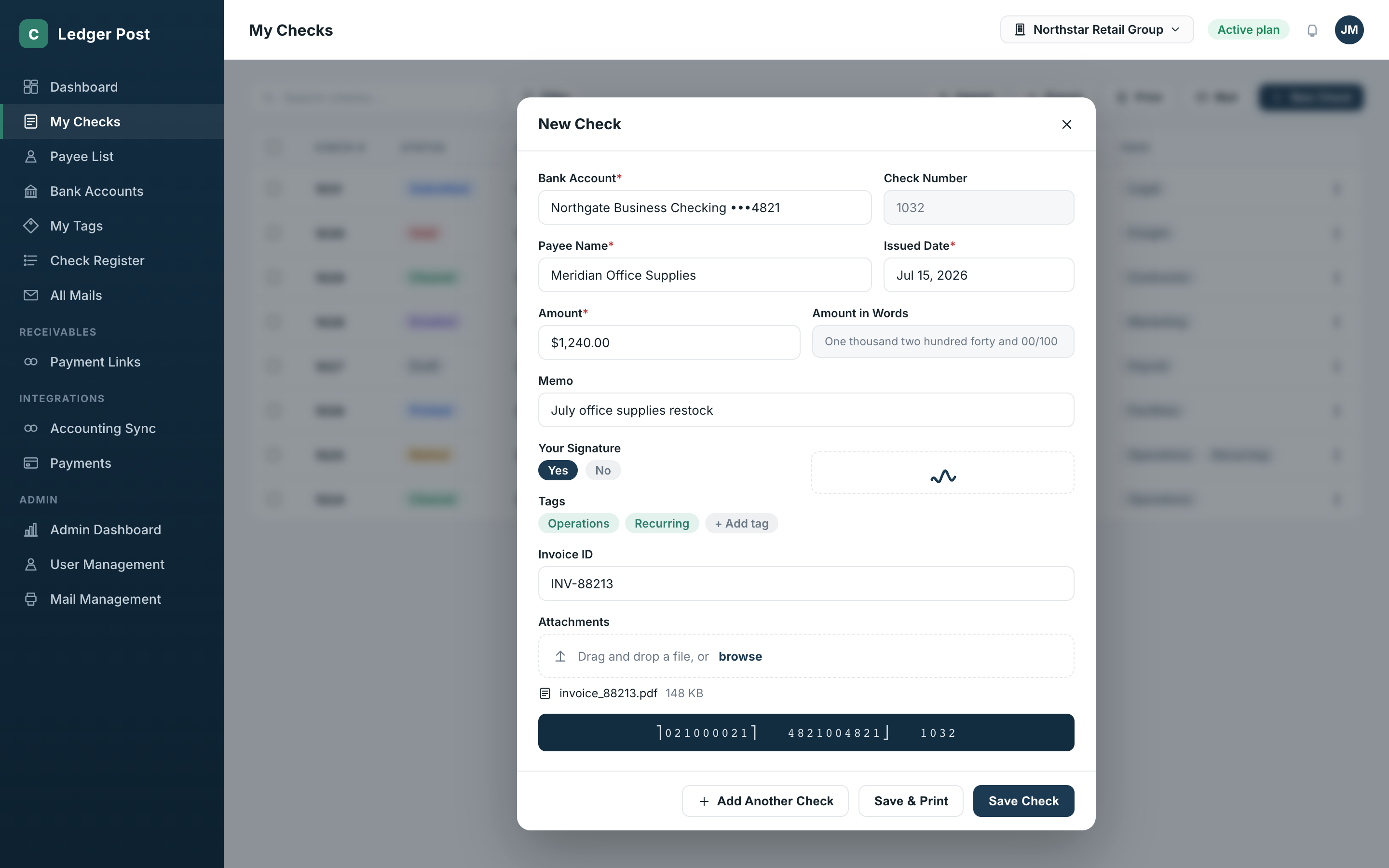

The heart of the product is the check-creation workflow, and it had to support two very different kinds of users: someone writing three checks a week, and a business writing hundreds. So a check can be created one at a time, with a live preview of the routing and account numbers rendered exactly as they'll appear on the printed document, or an entire batch can be queued up in the same sitting before anything is saved.

From there, the distribution choice is entirely up to the user. Some checks get printed on the spot. Some get emailed directly to a payee as a PDF. And some are handed off for physical mailing, where the platform takes over completely — printing, stuffing, stamping, and delivering the check through a fulfillment partner, with the small mailing fee billed automatically.

The Hard Problems Underneath the Surface

| Problem | How It's Solved |

|---|---|

| Taming messy, real-world data | Imports recognize and reconcile inconsistent spreadsheet headers automatically; every row keeps its original and corrected value side by side, is validated and staged before touching a real check number, and duplicate check numbers are caught automatically. |

| Keeping the books honest | Every create/edit/delete updates the ledger balance in real time with no batch jobs; every change to a check, payee, or bank account is captured in a permanent before/after audit trail, and deletions retire records rather than erasing them. |

| Visibility without chaos | Fine-grained, state-dependent permissions (a mailed check can't be edited from a stale screen) plus a genuinely separate administrator visibility layer that can't be reached by guessing a URL. |

| Cloud infrastructure that doesn't quietly break | Check PDFs, signatures, logos and imports live in cloud storage behind time-limited signed links; webhook notifications are independently verified against the untouched original request; checks render through the same browser engine used to preview them. |

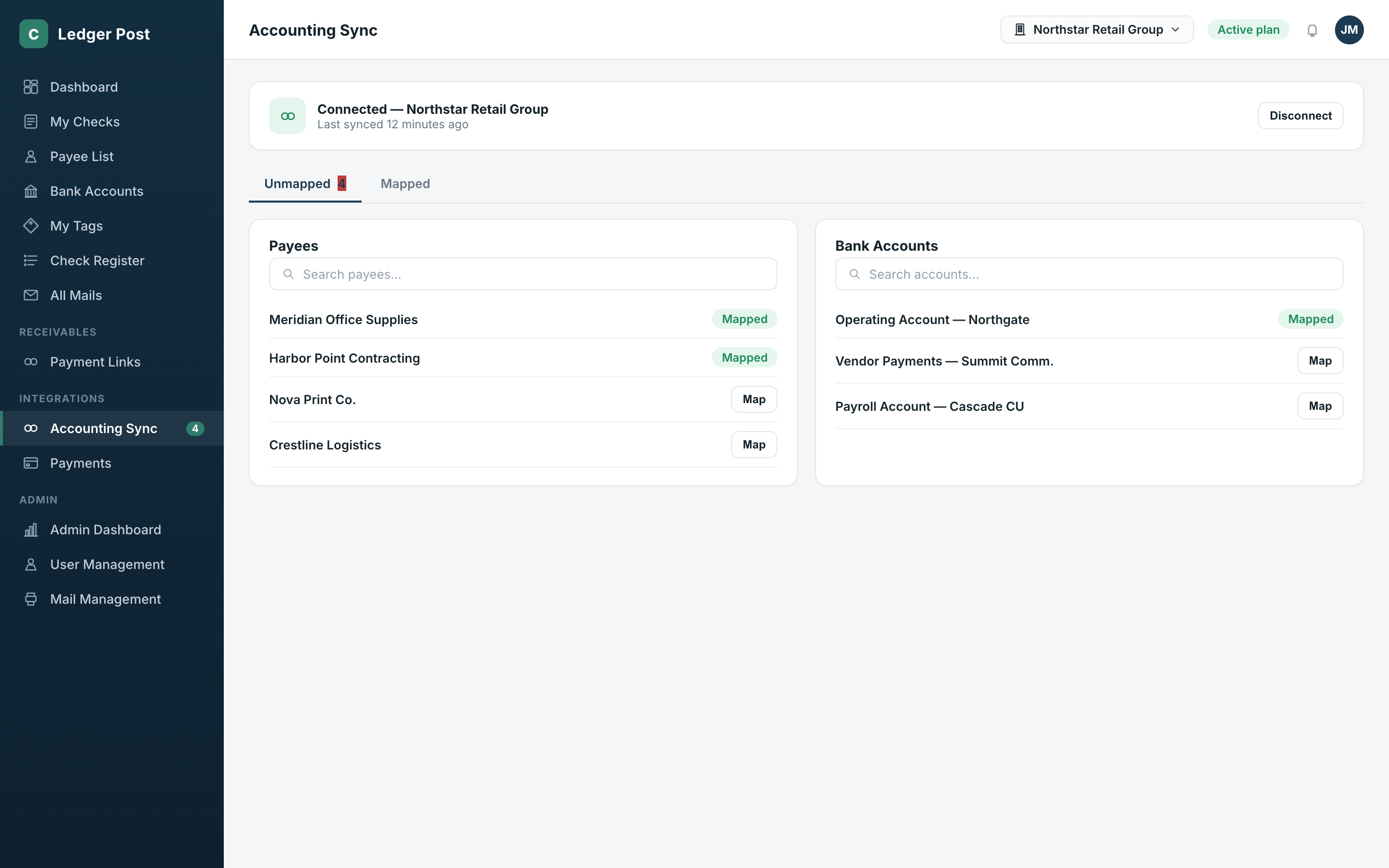

| Making external data speak the same language | A dedicated mapping layer keeps a persistent link between external and internal records while retaining the original external data, and treats "mapped" vs "unmapped" as a visible, countable state instead of a hidden background detail. |

| Notifications you can actually rely on | Verification codes ship over email, SMS, phone call, or an authenticator app; every mailing-pipeline stage triggers its own notification, and background checks flag stuck items and send a daily summary of what's still outstanding. |

| Security that doesn't get in the way | Session tokens refresh quietly before they expire, MFA is enforced as a server-side gate rather than a client-side assumption, and a short grace window avoids re-prompting for identity on every page load. |

Banks, Payees, Security, Payments & Admin Operations

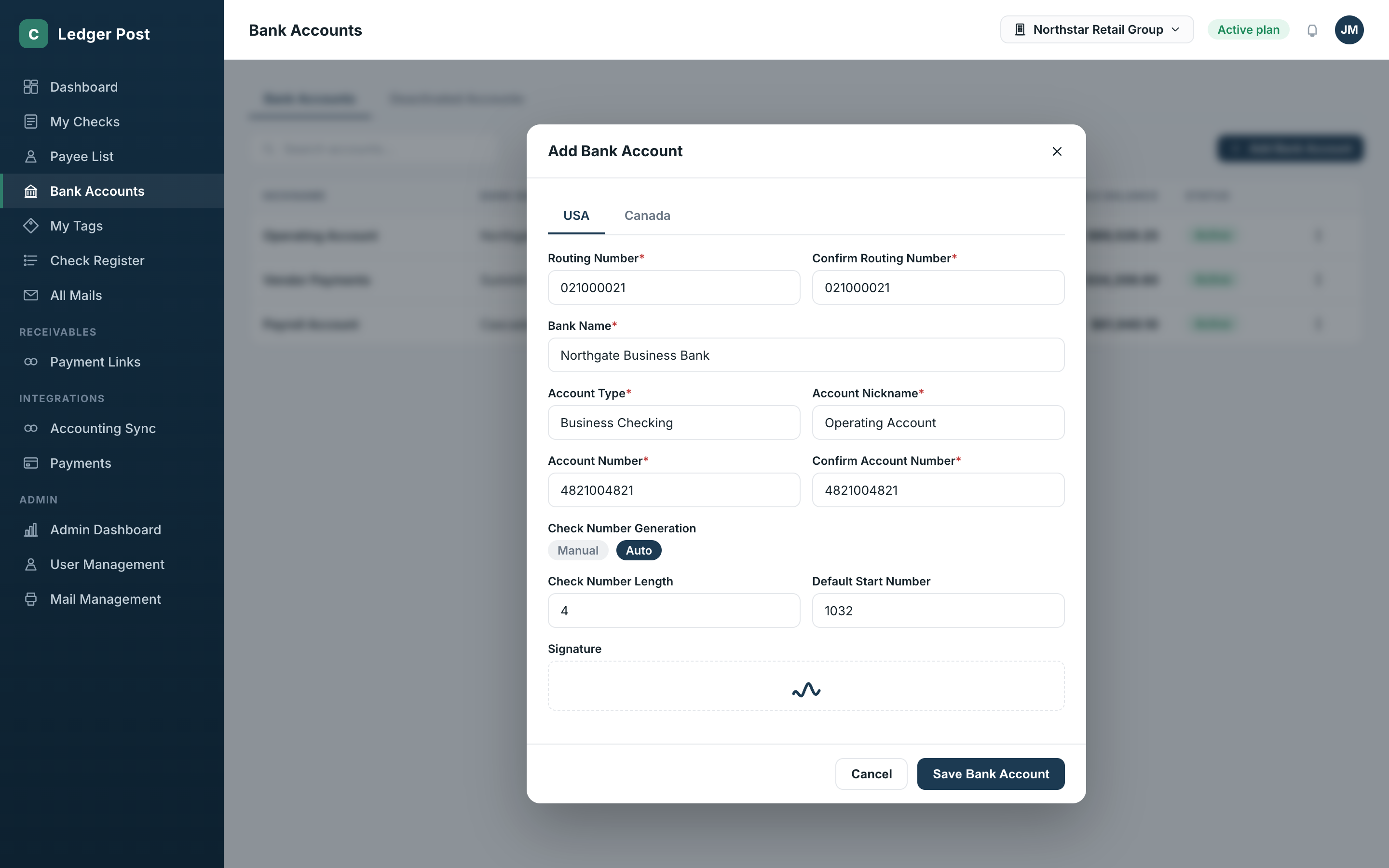

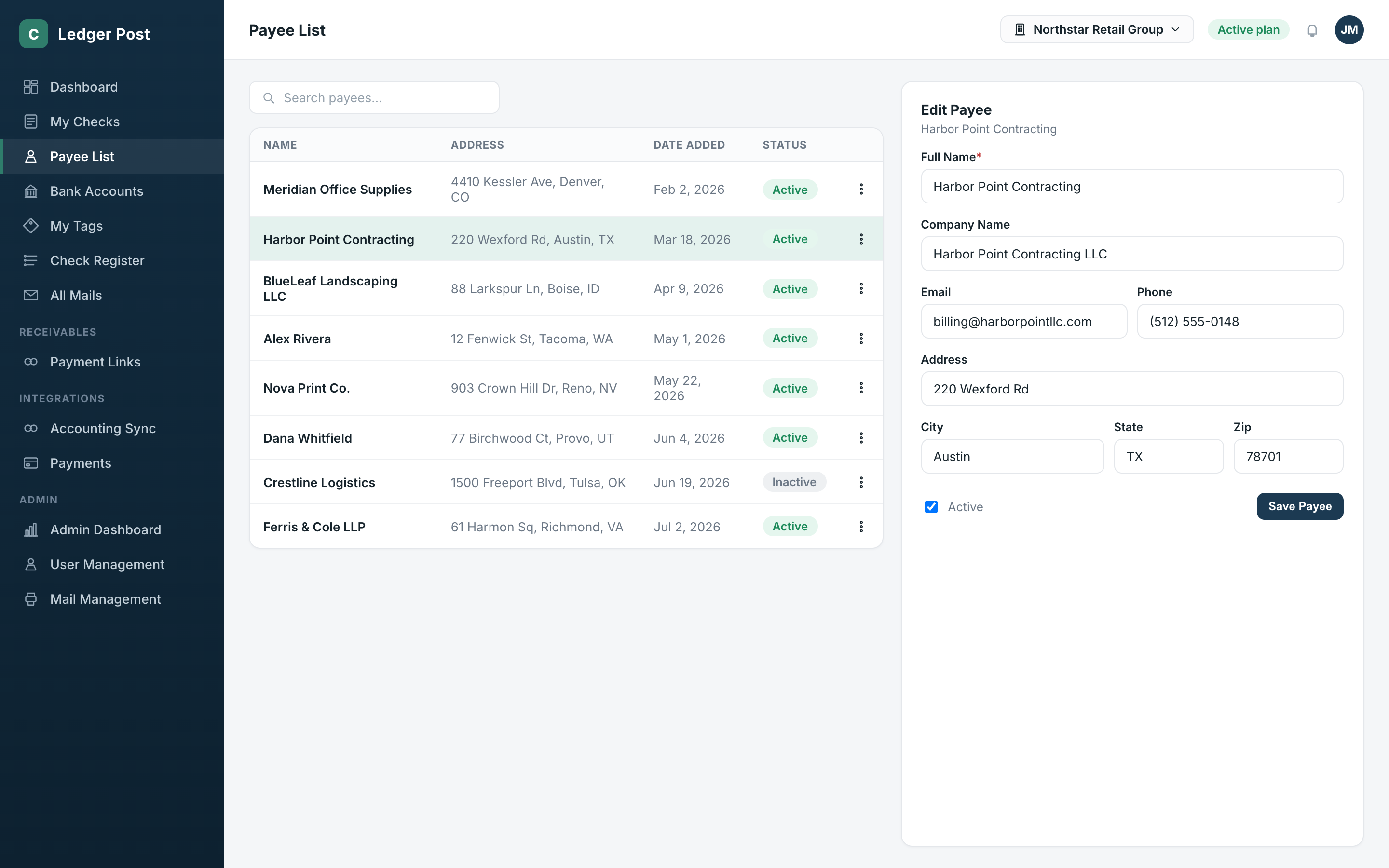

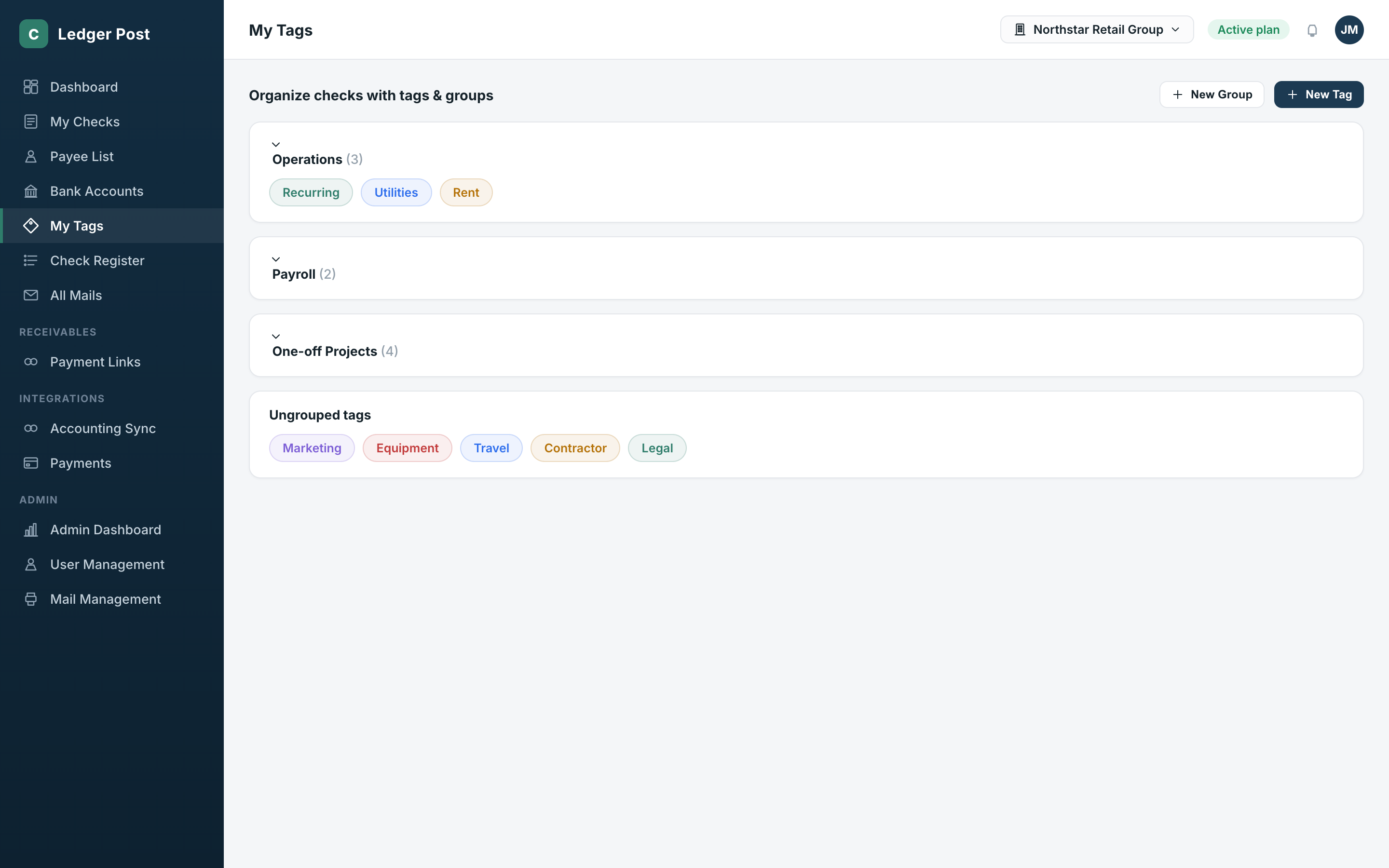

Behind every check is a bank account and a payee, and both needed to be first-class, well-managed records. Adding a bank account walks a user through routing and account numbers with confirmation fields to catch typos, and a digital signature — drawn, typed, or uploaded — can be attached once and reused on every check. Payees get a searchable directory with full contact and address details, editable inline. Checks can be tagged and grouped freely — recurring costs, one-off projects, departments — so filtering and reporting stay meaningful as volume grows.

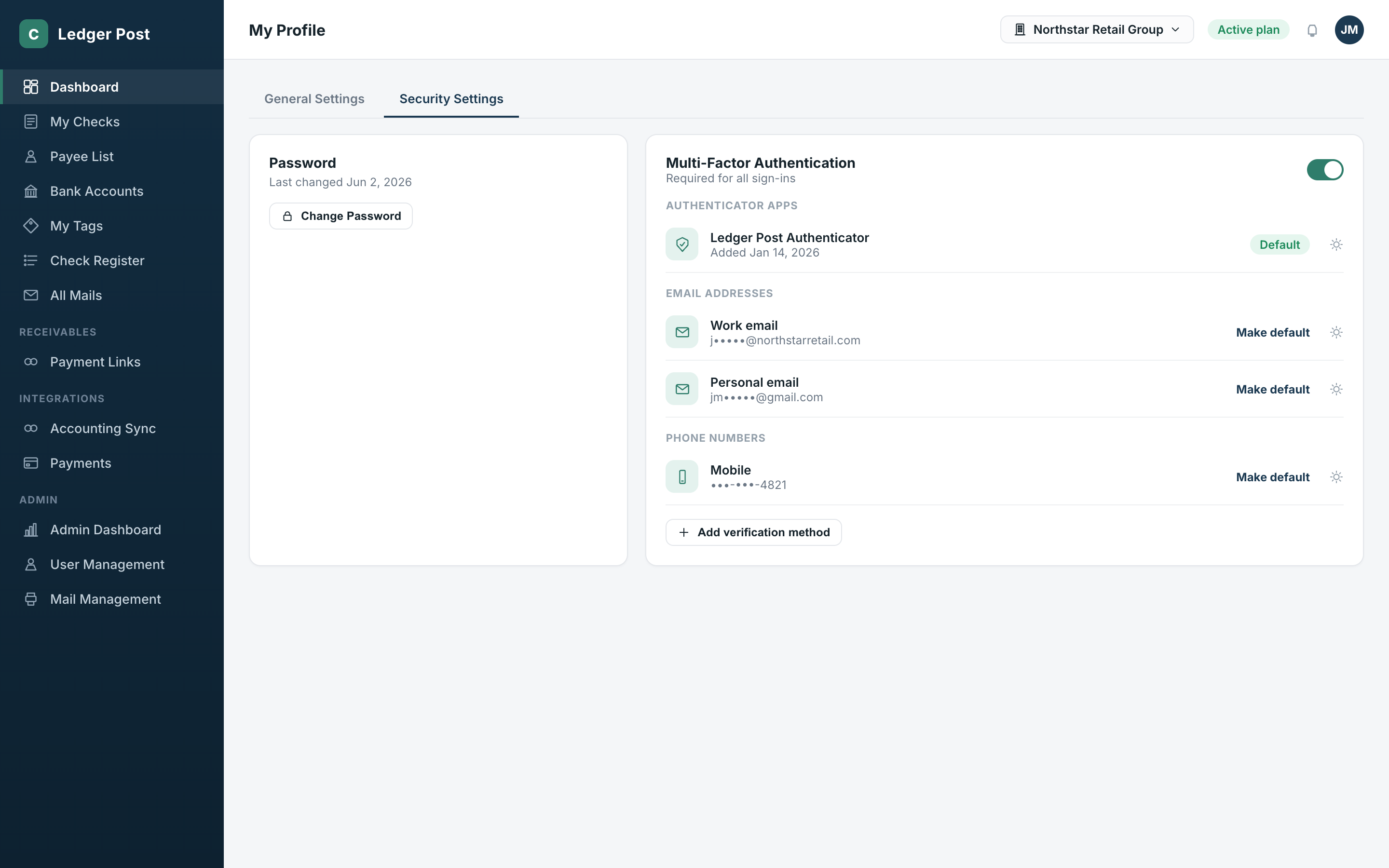

Security couldn't be an add-on screen buried in settings. The security area lets someone register multiple verification methods, see which one is set as default, and rotate their password on demand.

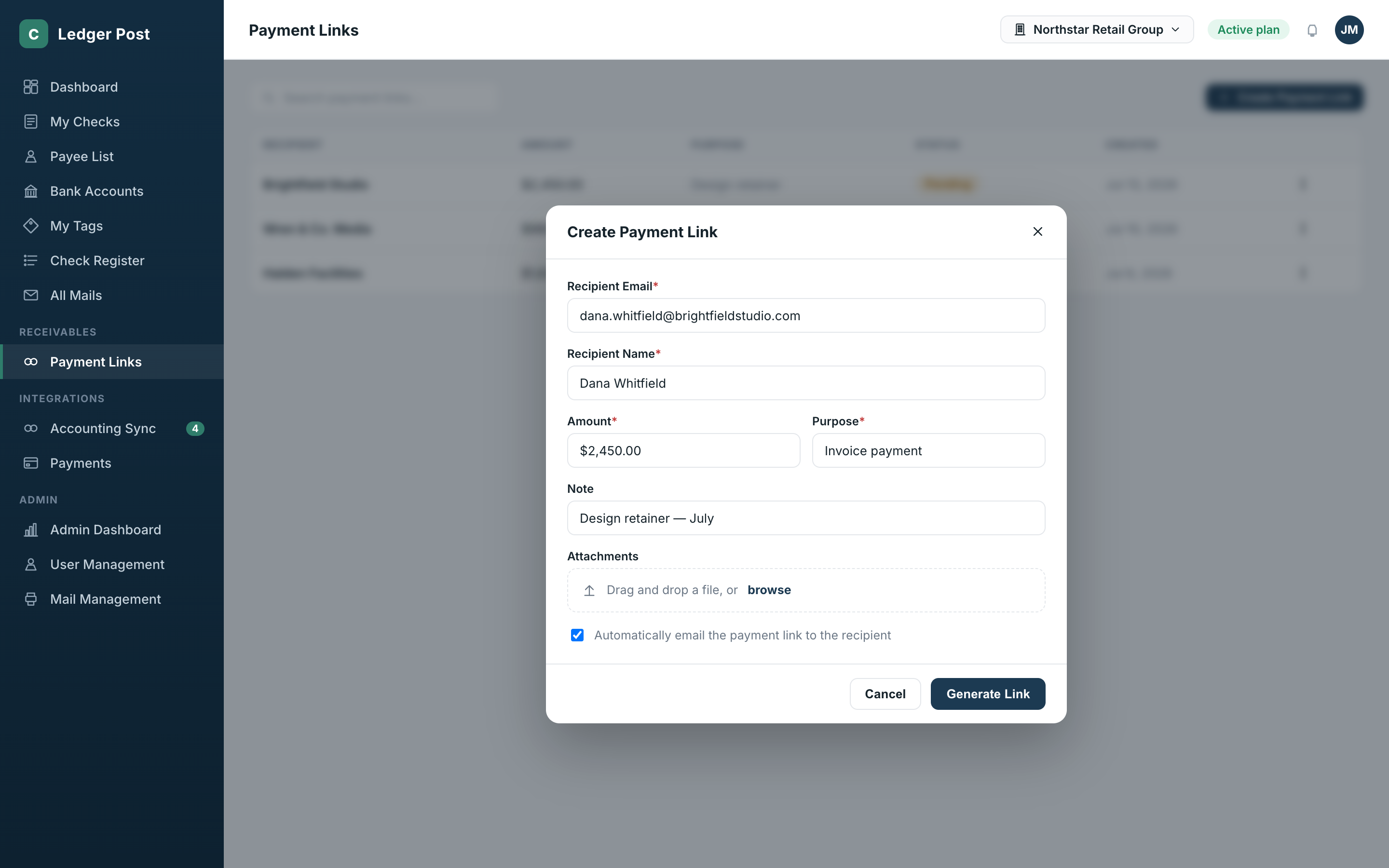

Every business that pays people also needs to get paid, so the platform includes a lightweight way to request money: a hosted payment link for a specific amount and purpose that a customer can pay by card, with an optional automatic email.

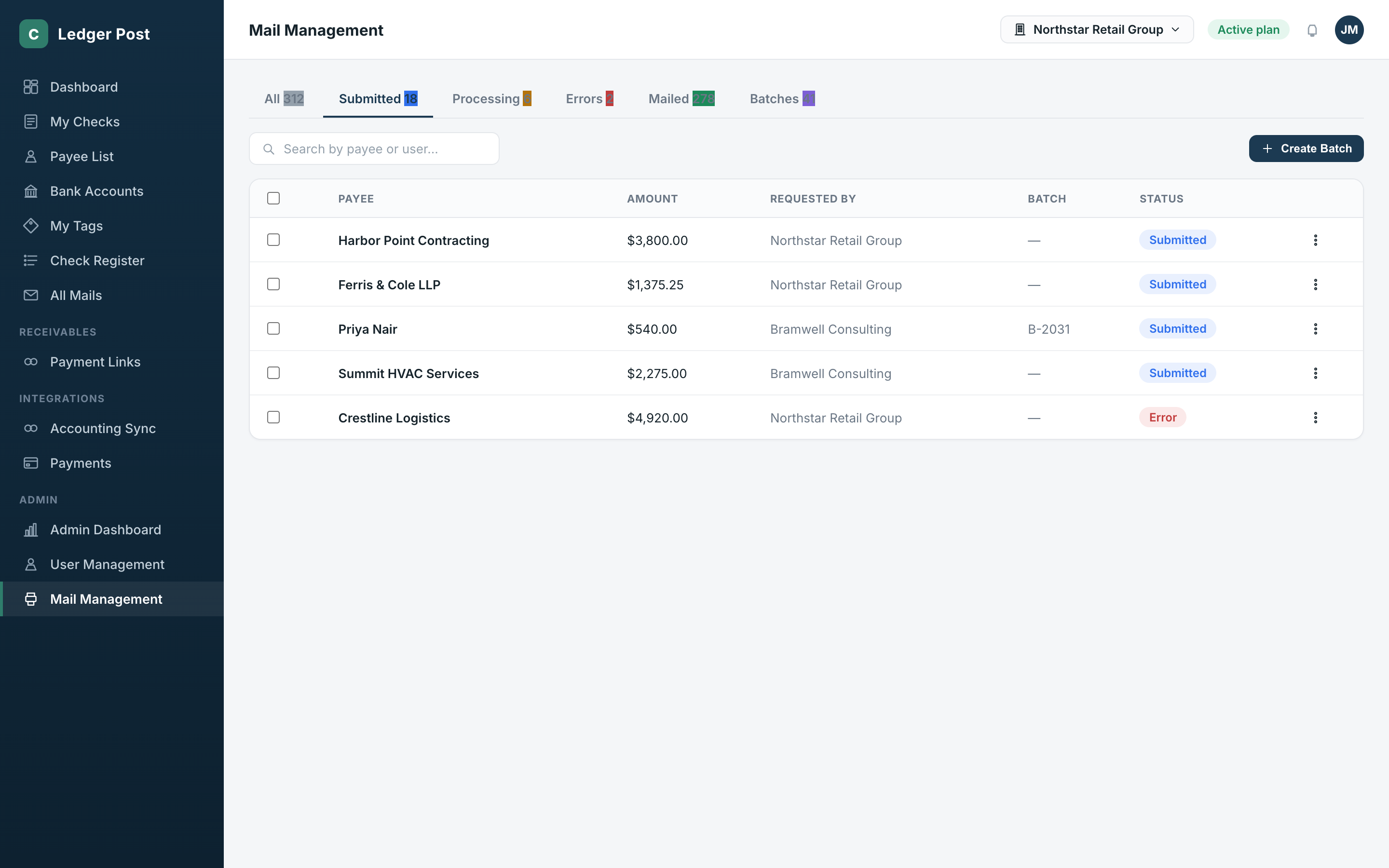

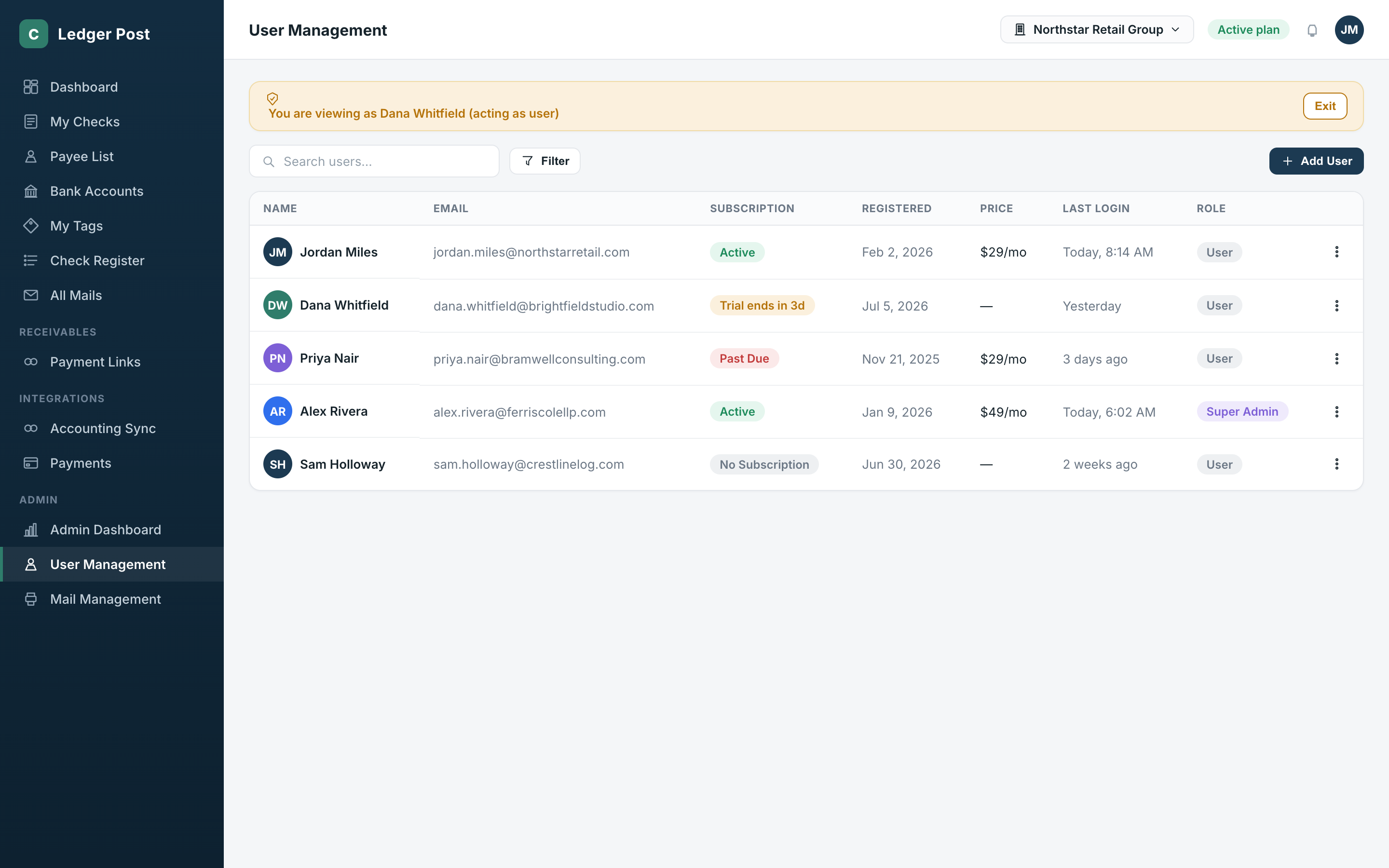

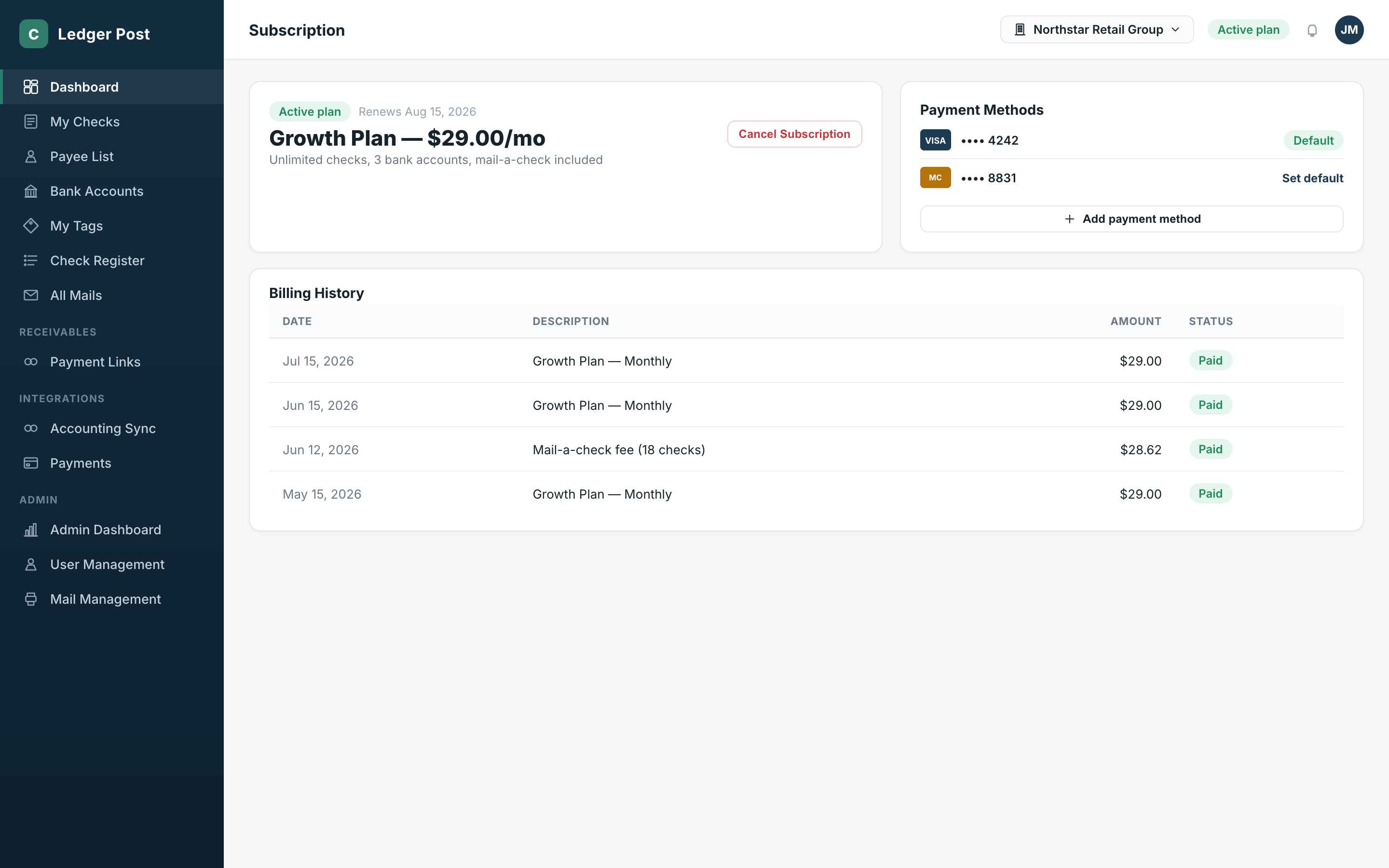

A direct sync with popular accounting tools lets a user map existing vendors and bank accounts to records already living in the platform, rather than recreating everything from scratch or maintaining two systems that quietly drift apart. Operations staff can track every check submitted for physical mailing, see where it sits in the fulfillment pipeline, and batch checks for printing. A full user-management console lets support staff reset a password, adjust a trial period, or securely step into a user's account to help troubleshoot — with an unmissable banner the entire time. Subscriptions and billing follow the same philosophy: a user can see their current plan, change payment method, and review past charges without opening a support ticket.

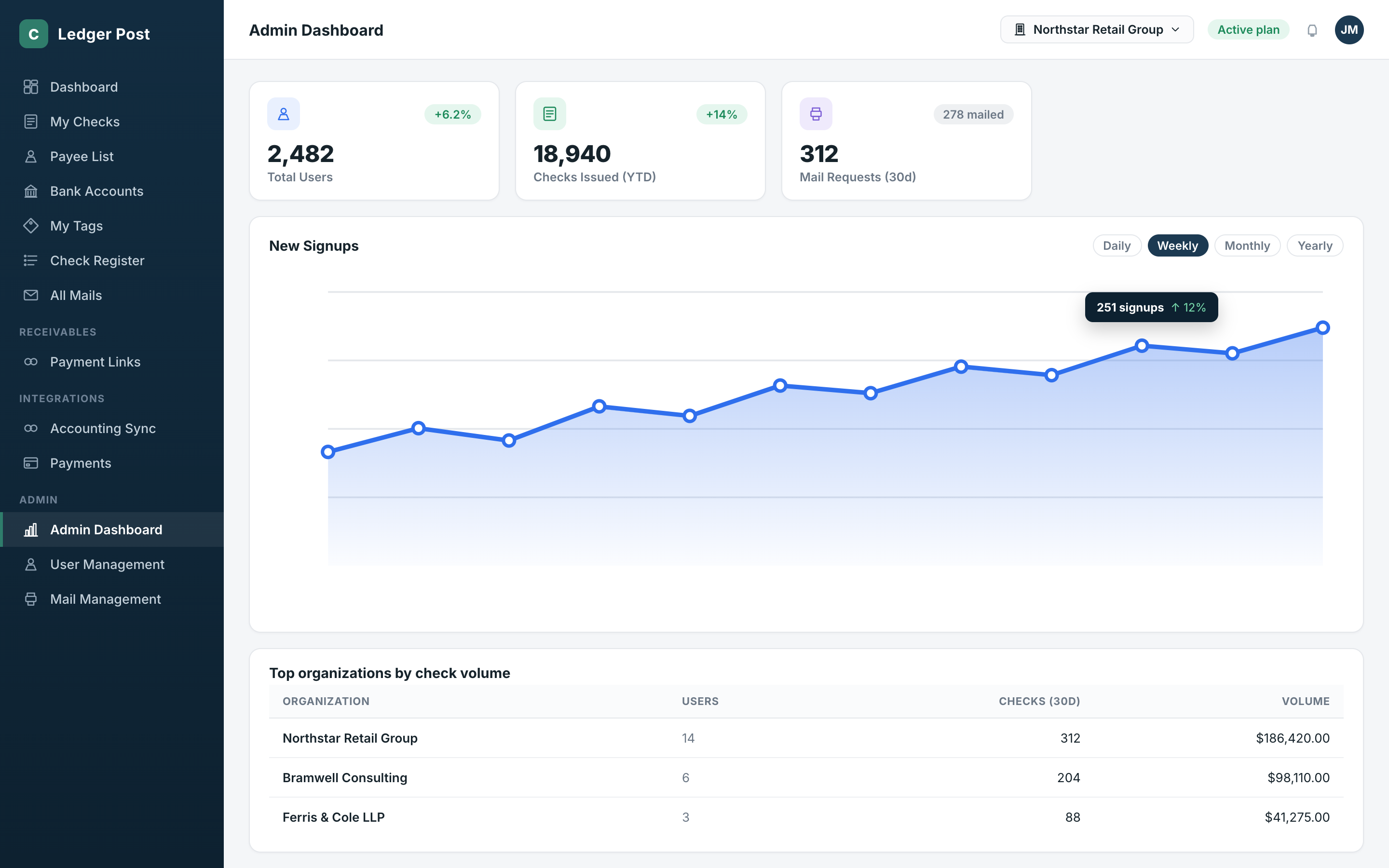

Operating at Scale: The Admin Side

None of this works at scale without someone able to see across the whole system. A broader analytics view gives leadership visibility into growth — signups over time, checks issued, and which organizations are driving the most volume.

The end result is a product where writing a check, mailing it, and watching the bank balance update afterward all happen as one continuous motion instead of three disconnected chores. On the other side, the team running the platform has full visibility into the mailing pipeline and account health without ever needing to touch the database directly.